Now just shy of 5 ½ years since it was launched, the VIX and More Newsletter continues to grow and evolve, with an increased emphasis on the volatility landscape, volatility products and related options trades since the beginning of the year. There was a time when investors only cared about the VIX and volatility when it was at elevated levels, but lately there seems to be as much concern about a low VIX as a high VIX and there is even some debate about whether the VIX is an accurate gauge of risk in the financial markets, a theme I address in Guest Columnist at The Striking Price for Barron’s: How to Spot Risk Early.

During the course of 2013, the newsletter has made a number of inroads into new territory, including:

- One area where the newsletter is always evolving is its coverage of volatility indices that cut across asset classes, geographies and sectors; the recent addition of the CBOE/CBOT 10-year U.S. Treasury Note Volatility Index (VXTYN) to the Volatility Update table and Volatility Overview section of the newsletter is one example of that trend

- Another enhancement to the Volatility Update table and Volatility Overview section of the newsletter is the use of sparklines to make it easier for readers to visualize where current volatility levels are relative to the range of volatility readings over the course of the past year

- A third enhancement has been a deliberate effort to focus on a greater number of trade ideas for each issue, to make those trade ideas more specific and less general, and to cast a wider net in terms of asset classes, geographies and sectors for those trade ideas

- While volatility ETPs and ETPs with an embedded options component continue to be one of the most important focus areas of the newsletter, I have recently made an effort to devote more attention to newer and lesser-known products in the VIX and options ETP space

- At the same time, I have also begun to include more analysis and discussion of VIX and volatility options trades and have also expanded the options component of the newsletter to incorporate the analysis and discussion of options trades for indices as well as ETPs in non-equity asset classes

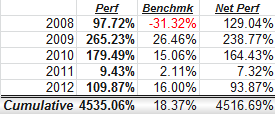

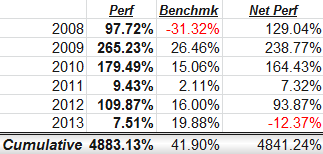

One of the most popular features of the newsletter since its launch has been the Stock of the Week, which has posted head-turning numbers in four of the six years it has been operating. As the table below shows, the performance for the Stock of the Week in 2013 has not lived up to historical standards and I have no particular explanation for why 2011 and 2013 show significantly lower returns than the other four years. Of course, with a single stock ‘portfolio’ whose average weekly change is 5.0% per week, there is necessarily a huge variation in returns, particularly for measurement periods of less than one year.

[source(s): VIX and More]

Please note that as is the case with EVALS performance data, going forward I will no longer be publicly updating Stock of the Week performance data due to a variety of factors related to the launch of my new investment management business. I will continue to offer the newsletter service and the Stock of the Week selection (details below) and will be pleased to discuss current performance data privately. Also, as soon as the launch of my new investment management business is finalized, I will highlight some of the particulars in this space.

[For those seeking additional information on the newsletter, I am offering a 14-day free trial (see top of right column) to the subscriber newsletter for all new subscribers. Additionally, for those who may be interested exclusively in trading VIX ETPs, my VIX and More EVALS (ETP Volatility Analysis Long-Short) model portfolio service is certainly worth investigating. Feel free to contact me at bill.luby[at]gmail.com for more information about the newsletter or EVALS.]

Related posts:

- Q4 2012 Newsletter Update, with Stock of the Week +109% for 2012 and +4535% Since Inception

- Q3 2012 Newsletter Update, with Stock of the Week +107% YTD and +4473 Since Inception

- Changes to Newsletter Place More Emphasis on VIX Exchange-Traded Products

- Highlighting Newsletter Content Focus with Content Pyramid

- Newsletter and Portfolio Performance Update Through 12/31/10 (includes a discussion of the Stock of the Week)

Disclosure(s): none