The first change is relatively straightforward. Acting on quite a few requests for more analysis VXX, I added my proprietary VIX Futures Contango Index to the Volatility Update table I publish each week in the recurring Volatility Corner section of the newsletter. Each week I now review the VIX futures, the VIX Futures Contango index and the VXX roll yield in the context of their impact on VXX and other volatility products.

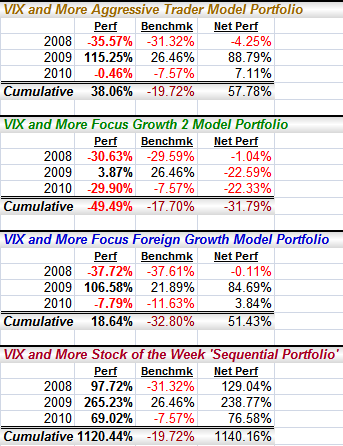

The more substantial change involves changes to the Focus Growth 2 model portfolio. After two years of disappointing performance, I decided to revamp both the stock selection rules as well as the position management algorithms. The changes result in a model portfolio that places increased emphasis on greater long-term growth potential and recent earnings growth, as well as an attractive valuation and volatility profile. The net result is a model portfolio that more closely resembles another portfolio I have been managing in real time for five years that has an average annual return of 39%. It is my intent not to jettison this underperforming model portfolio, but rather to accept the challenge to work to make it a benchmark-beating performer, just as the other two model portfolios have been.

This brings me to the performance data below. All three of the model portfolios topped their benchmarks during the quarter, with the changes to Growth 2 responsible for about a 3% advantage over the benchmark S&P 500 index during the last month of the quarter.

Every time I post this data, invariably the big story becomes the Stock of the Week ‘Sequential Portfolio’ (SOTW) and its 91% gain for the first three quarters of 2010 and 1281% gain since its March 30, 2008 inception. I should probably reiterate what I said last quarter, notably that Michael Stokes of MarketSci had a three-part series in which he reviewed the SOTW, first as a single stock portfolio, then using a short SPY position to hedge market risk and finally examining a theoretical 10-week holding period. The quick summary of MarketSci’s findings is that the performance of the SOTW is very strong both unhedged and hedged, but there is not convincing evidence of persistent outperformance past the initial post-selection week.

The full set of MarketSci reviews can be found at:

- Review of the VIX & More Stock of the Week

- Hedging the VIX & More Stock of the Week – uses a short SPY position to hedge market risk, with impressive results

- Holding V&M’s Stock of the Week for Longer than a Week – looks at a 10-week holding period and does not find persistent outperformance past the initial post-selection week

“This is different from the Friday close to Friday close data I have always reported in my subscriber newsletter, because I always wanted to report a cost basis in the newsletter on Sunday and assumed that if I avoided stocks which had news over the weekend, the difference between using a Friday close vs. a Monday open as a cost basis would not be meaningful in the long run.”For those seeking additional information, I am offering a 14-day free trial (see top of right column) to the subscriber newsletter for all new subscribers.

Disclosure(s): short VXX at time of writing